Published on June 26, 2025 9:17 PM GMT

Even if we get ultra-capable frontier models, we’ll need lots of GPUs to run them at scale. Currently, our installed GPU stock isn’t enough to automate the white-collar workforce or cause extinction. We need more!

Tyler Cowen thinks we should predict AI progress using asset prices. He’s usually thinking about interest rates, but what about NVIDIA’s stock price? Since NVIDIA makes almost all of the GPUs used to train and run AI models, and since GPUs generate almost all of NVIDIA’s sales, NVIDIA’s market capitalization basically represents the discounted value of future cash flows from the GPU market.

Using a reverse DCF model, you can estimate how much NVIDIA must grow to generate cash flows consistent with their current valuation. Since NVIDIA generates cash flows by making sales and generates sales by making GPUs, you can back into a global GPU projection by making further assumptions about margin, price, and market share.

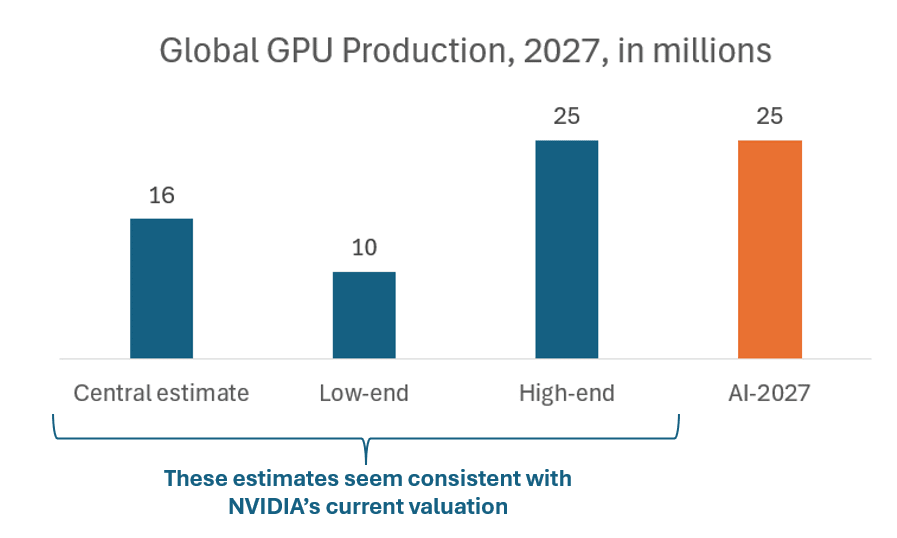

In that spirit, I modeled an explicit GPU production forecast based off of NVIDIA’s valuation. In their background research, the AI 2027 folks also make explicit predictions about GPU production in their compute forecast. Do thier assumptions imply that NVIDIA is under-valued? Looking just at 2027, it’s pretty hard, though not impossible, to reconcile the AI 2027 assumptions with NVIDIA’s current valuation. One could argue that the conclusion “Daniel Kokotajlo should buy NVIDIA stock” is less than revelatory, but I will nonetheless continue writing this post.

First, how did I get these numbers? For 2027, it was pretty easy, because I rely on a consensus forecast for near-term financials. Equity analysts are generally expecting NVIDIA to have $250 billion in net sales by 2027. The price of an H100 GPU is $25k, so you might think that implies ~10 million GPUs. My central estimate is higher, because I assume some reduction in price and some decline in NVIDIA’s market share. Here’s the actual math behind my 16 million central estimate for 2027:

$250 billion net sales

x 92% of sales are GPUs

x (1 / $18k GPU unit price)

x (1 / 0.8 NVIDIA market share)

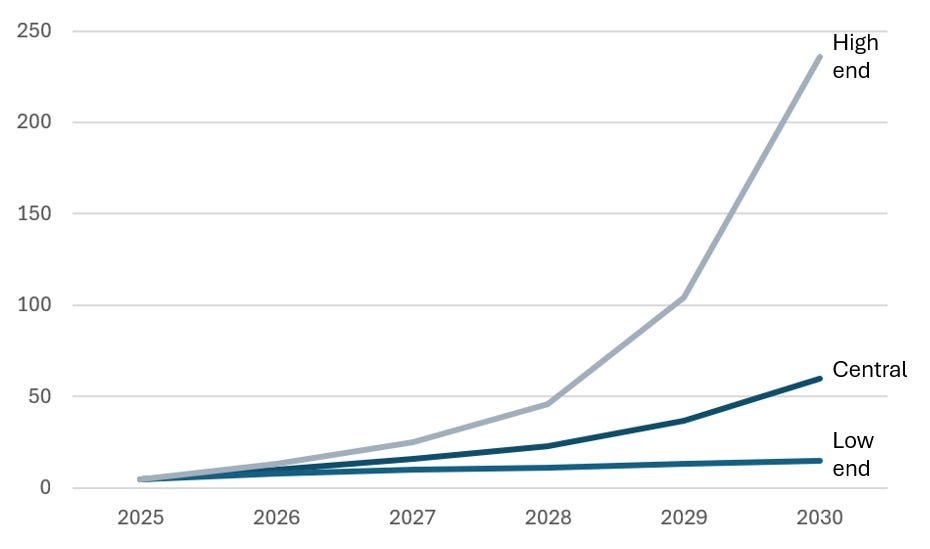

The consensus forecast only runs through 2028, so my spreadsheet goes a little further by projecting what growth you would need through 2035 to justify NVIDIA’s market cap. Things get very uncertain very quickly. It seems like NVIDIA’s price is consistent with production being somewhere between 15 million and 250 million GPUs by 2030. By 2035, I’ve nailed it down to somewhere between 30 million and 30 billion.

Forecasted annual GPU production levels, in millions, 2025-2030

Why is my range so big? Here’s the mix of assumptions that defined my low end and high end scenarios:

- Discount rate (10%-13%). Higher discount rates imply higher near-term sales. The low end implies NVIDIA is lower risk than a typical semiconductor company, whereas the higher end is what CAPM spits out when you plug-in NVIDIA’s beta.2025-2029 cash flow growth (15%-28%). I calibrated these using a reverse DCF model. Basically, I treat this as my one free parameter, and set it to whatever it needs to hit NVIDIA’s market cap.Post-2035 cash flow growth (2%-4%). Lower rates imply higher near-term sales, because lower long-run growth requires you to front-load sales growth to hit the cash flow target. 2%-4% is the typical range used for DCF models.Decline in margin. Lower margin implies higher near-term sales, because it means you need more sales to hit the cash flow target. My low end scenario assumes NVIDIA keeps their current sky-high margins, whereas my high end scenario assumes NVIDIA falls to commodity margins by 2035.Annual change in GPU prices (0% to -30%). Lower prices imply higher near-term GPU production, because you need to sell more units to hit the cash flow targets. I estimate that real prices for A100s, the H100 predecessor, have declined by about 15% per year, so I base my range on that.Share of NVIDIA growth driven by GPUs. Technically, not all of NVIDIA’s sales come from GPUs, but pretty much all of them do, so this assumption doesn’t move the needle much.Decline in market share. Lower market share implies higher global GPU production, because NVIDIA’s valuation is only measuring a fraction of total production. My low end scenario assumes NVIDIA keeps 90% market share, but my high end scenario assumes their market share drops to 20% by 2035.

You could try to narrow the range some by structuring this as a Monte Carlo simulation, treating some parameters as independently drawn, and allowing some of the uncertainty to cancel out. But you can’t escape the core challenge of this exercise, which is that NVIDIA’s valuation is consistent with two very different scenarios that imply very different GPU production levels:

- Scenario 1: NVIDIA monopoly. Investors expect NVIDIA to retain its moat, NVIDIA keeps market share, margins stay high, and prices stay high. This will let NVIDIA generate massive cash flows for shareholders, despite not producing many GPUs.Scenario 2: GPU commodity. Investors expect competitors to replicate NVIDIA’s advantages, causing NVIDIA to lose market share, margins to collapse, and prices to drop. Yet, the GPU market grows so unfathomably large that NVIDIA still generates massive cash flows for investors.

Considering these scenarios illustrates a further problem with my approach, because investors might believe both outcomes are possible. My method assumes that investors are valuing NVIDIA based on some kind of central forecast. But a lot of investors might be averaging across discrete scenarios of varying likelihood. In the most extreme case, maybe investors think AI is probably hype, but there’s a small chance of a singularity where NVIDIA shareholders rule the Earth, and most of the valuation is driven by that tail outcome. In that case, my numbers are junk.

Building this model, I felt a connection with Homer Simpson and his barbeque pit building experience. Why is life so hard? Why must I fail at every attempt to make something useful? Before I started this exercise, I was surprised that I couldn’t find similar attempts from others. Now I understand why: predicting concrete outcomes from stock valuations just doesn’t work very well.

Discuss