Michael J. Fiedler for BI

Noah Sheidlower spent two days following Lydia and Bill Hinds, a married couple of nearly 30 years, who say they're just scraping by in central Connecticut. He reviewed their financial records for this story. He also interviewed more than 90 workers in their 80s and 90s, and 30 researchers and nonprofit leaders focused on older Americans at work. This story is part of a series on people working past 80.

Lydia Hinds, 81, collapses onto her red couch, takes a deep breath, and lets out a defeated yell.

She just returned home from what was supposed to be a five-hour shift wiping down appliances and helping customers at a Home Depot in Berlin, Connecticut. In the first four hours, she paused several times to catch her breath, so she clocked out an hour early.

"I feel trapped working, but I can't stop working," Lydia says, sitting up to cuddle her basset hound, Brigette. Her husband, Bill, gives her a kiss but lets her be. The 90-year-old would like to get a job to help Lydia pay the bills, but because of health problems, there's little he can do.

"I feel so guilty that I can't work," Bill says.

"You can't work because of your age and your health issues," Lydia snaps back. "There's no sense feeling guilty about it."

Michael J. Fiedler for BI

A certificate for a regional award that Lydia received from Home Depot, praising her dedication to the job, sits on their coffee table. Since starting in 2022, she's received two promotions, despite being unable to climb ladders or lift heavy objects because of her heart failure diagnosis last year. In a photo attached to the award, she's smiling from ear to ear. Now, the best Lydia can muster is a muted grin.

If she stopped working and lost her $300 weekly pay after taxes, she and Bill fear they couldn't afford rent. A few weeks back, they had 44 cents in savings. They weren't sure what they would eat for dinner.

Three printed-out job applications for remote customer service positions lie near her award. She doubts she'll get further than one interview, but each application is a glimmer of hope. "What company would hire an 81-year-old?" Lydia asks. "Hopefully one of them."

A better-paying, less intense job could give them the boost they've yearned for, especially as Lydia's weekly hours some weeks have been cut from 22 to 17.

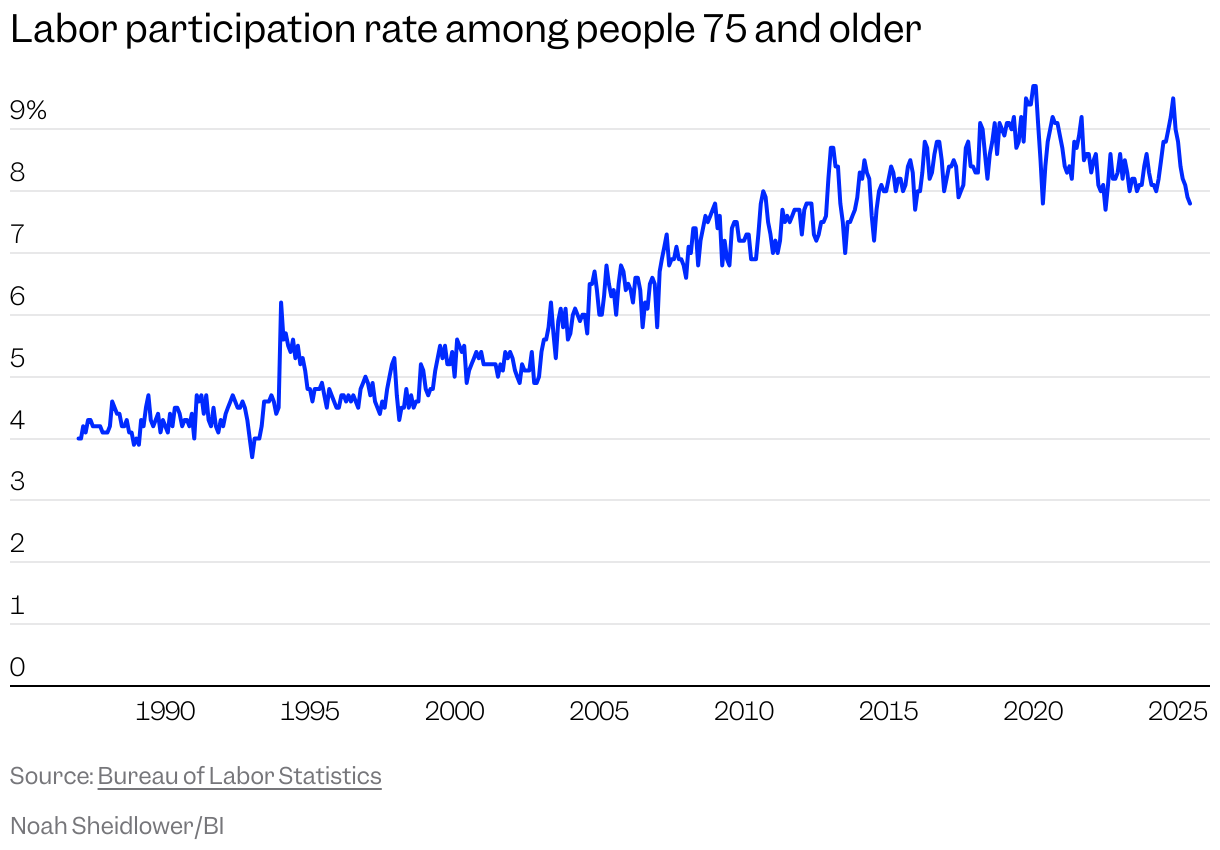

Lydia is one of over half a million Americans over the age of 80 who still work as managers, retail salespeople, lawyers, drivers, and other jobs — over 4% of the Silent Generation. That number has gone up to 4.2% from 3.6% in the last decade due to various factors making full retirement impossible or undesirable for a growing number of seniors, according to a Business Insider analysis of Census data.

"We do know that the 75-plus demographic is the fastest growing segment of the workforce," says Carly Roszkowski, vice president of financial resilience at AARP. Americans age 75 and over are twice as likely to be in the workforce now as they were in the early 1990s, according to Bureau of Labor Statistics data.

Those in their 80s or older are part of the Silent Generation of Americans born between 1928 to 1945. They grew up against the economic backdrop of the Great Depression and World War II, and learned to be financially cautious after seeing what their parents endured. However, they didn't have access to the same kind of personal finance advice and tools that are prevalent today.

Michael J. Fiedler for BI

In recent months, more than 90 workers aged 80 and older told Business Insider in interviews how health challenges, loneliness, and increased cost of living all play into their decision to work at their age. Over a dozen say all they could find were minimum-wage jobs, and many work despite medical diagnoses. The financial strain bleeds into their relationships with spouses and children, and exacerbates a pervasive feeling of isolation.

Right now, the Hindses take in $4,600 a month from their Social Security, Bill's pension from a TV station in Connecticut, and Lydia's monthly wages. Monthly rent for their one-bedroom apartment in a 55-plus development is $1,400, their car payment is $625 a month, their car insurance is $236 a month, and their Medicare combined is $426 a month. On top of that, they have emergency medical expenses, medications, grocery and gas bills, and utilities. They're left with close to nothing at the end of the month.

"I keep thinking, 'What happened that we can't go out?'" Lydia says of the couple's social life. "But the rent's gone up, and it's eaten up most of the Social Security money. We're in deep trouble."

Healthy enough to work into their 80s

Bill and Lydia say their financial mistakes were ones anyone could make. They never gambled, their investments weren't too risky, and they worked in decently paid jobs their entire careers.

Still, some miscalculations, unavoidable health issues, and poor timing have put them in a wobbly financial situation.

"Every month when it's time for my Social Security check, I get really tense. I'm so afraid it's not going to come," Lydia says. "If we don't get that, we're out of here. We're on the street."

Michael J. Fiedler for BI

The number of cost-burdened households — those that spend more than 30% of their income on housing expenses — age 65 and older has steadily risen since the early 2000s. Research from the Joint Center for Housing Studies at Harvard University found that among adults age 75 and older who live alone in metro areas, only 13% could pay for assisted living without having to dig into their assets.

"I wish I had saved just $20 a week in my retirement account all those years ago," Lydia whispered during her shift. Even a small nest egg would relieve her stress. She has under $1,000 left in her 401(k) from Home Depot, down from nearly $10,000 at its peak, as she pulled out money twice for medical and day-to-day costs.

In 2022, Bill and Lydia needed additional income. During the pandemic, they'd both suffered from health issues, including Bill breaking his leg, which kept them from working. They relied solely on Social Security, Bill's small pension of $335 a month from his time at the local TV station in advertising sales, and some savings. But when they couldn't sustain their lifestyle anymore that year, Lydia drove down the road to the closest Home Depot and applied for a job. Home Depot hired her at $16 an hour in the electrical department. She was 79.

Michael J. Fiedler for BI

"I loved it at first, and I still enjoy my customers," Lydia says. "But when I started there, I didn't know I had heart failure."

When Lydia noticed tasks like sewing curtains and gardening knocked her out, a doctor found that her heart was not pumping nearly enough blood. At work each day, she's expected to clean appliances, keep aisles tidy, and help customers with their needs for $19.55 an hour. Still, she kept her sense of humor.

"When I got the echocardiogram, I joked with the doctors and told them, 'I forgot to tell you I'm pregnant,'" Lydia says. "They got a big laugh out of that."

As her condition worsened, she would have to catch her breath just from walking down an aisle. Conversations with customers and coworkers, who call her "Ms. Lydia," keep her ignited.

She says she's thankful that Home Depot has given her time off with pay, as part of her sick leave benefits, to go to doctors' appointments. She used Connecticut's paid family medical leave for six weeks because of her heart failure diagnosis.

Home Depot didn't respond to a request for comment for this story.

Lydia isn't alone in her battle between work and health. Similar circumstances have pushed many of those who are healthy enough to continue working. Others in her position may need the income, but aren't physically able to work. Beth Truesdale, a research fellow at the W.E. Upjohn Institute for Employment Research, says a "shocking number of people" are pushed out of the labor force in their 50s and 60s, let alone their 70s and 80s.

Michael J. Fiedler for BI

The percentage of people who are working drops sharply starting around age 51, across all genders and education levels. Truesdale's calculations from 2020 showed a roughly 20-point fall in the percentage of people working at age 61 compared to 51. That's not mainly because of early retirements, she says. It's because of factors like poor health, caregiving responsibilities, and physically demanding roles.

Dozens of older Americans told BI over the last year that they had no choice but to retire earlier after a diagnosis or injury. Many rely solely on Social Security, which is about $2,000 monthly on average.

Lydia's coworker, Tony Sparveri, 80, works for a similar reason as her. He started part-time at Home Depot two decades ago in the gardening department before transitioning to a full-time kitchen and bath design consultant. He's not on his feet all day, and says the work makes him feel youthful. He earns more than Lydia and works mostly for financial reasons, as taxes on his home and rising costs have burdened him and his wife.

Michael J. Fiedler for BI

"Mentally and physically, I feel really good, and that's a blessing," Sparveri says. Still, he's concerned that many older people will continue to be hurt by rising prices and economic uncertainty. "People are suffering, and I don't want to put myself in that position."

Love keeps them going through financial ups and downs

One afternoon, Lydia searches every nook and cranny of the apartment in search of a CD by Bill's former jazz ensemble, recorded in 1996 with jazz pianist Bill Mays.

"It's blue and yellow. I've looked everywhere," Lydia calls out to Bill. "There's no way I lost it!"

He walks to a cabinet and pulls it out. She puts it into the CD player and starts dancing, humming the melody to the first track. Bill looks on with a slight smile. He started playing piano when he was 3, performed with a swing jazz band, and hosted an FM jazz radio show in Austin.

"Most of those people are dead," Bill says of his old bandmates.

"Well, you're not," Lydia quips.

Bill and Lydia have lived in their current apartment for six of their nearly 30 years of marriage. This is Bill's second and Lydia's third marriage, and each has children from previous spouses. Lydia lost much of her savings in her 40s when her second husband abruptly closed one of the successful office and mail service stores they started together. He declared bankruptcy very shortly after.

Michael J. Fiedler for BI

"It all went down the tubes," she recalls, noting she was able to get a previous job back shortly after. "I still don't know how I got through that."

They didn't know each other at the time, but while Lydia was recovering from that financial setback, Bill was making $90,000 a year from performances and his work at the TV station. Lydia met Bill through a dating service in 1995. He picked her up for their first date in a white limousine, wearing a camel-hair coat.

"I was going on dates with three women at the time, but when I saw her, I dropped them all," Bill says.

"He had glasses three times bigger than he needed, which I took care of," Lydia jokes.

Like any marriage, theirs has had its ups and downs. After a brief stint in Florida, they returned to Connecticut and spent most of their savings on a house that required more repairs than they had expected. Lydia had moved on from the now-closed mail stores and was working as a real estate agent, but says she rarely made enough money to be comfortable. Bill had left the TV station in 1994 to focus on his band and was playing at weddings, teaching piano lessons, and selling pianos. They had been able to save a little throughout their career, but never enough to think they could retire.

"We put almost all of our money into that house," Lydia says. She says they bought it for $185,000 in 2002 and spent more than $100,000 on renovations. "It looked a lot better, and we figured we'd flip it and do OK."

Then the 2008 recession hit "like a ton of bricks," Bill says.

At the time, they had $75,000 invested in the market, but as the market fell, they pulled from their account to pay for their increased mortgage and property taxes. The couple hoped they'd get some money out of the home they'd renovated. But they defaulted on their mortgage in 2015, and a forced sale brought only $115,000. They filed for bankruptcy. The income from a side business Lydia had started to help people downsize their homes, and the piano lessons that Bill gave, weren't enough.

They were among the more than 10 million Americans who lost their homes due to the Great Recession. The S&P 500 took over five years to fully bounce back after dropping more than half its value from its high in 2007 to its lowest point in 2009. For thousands of households approaching retirement age, this meant working longer after their savings shriveled.

"I take a lot of responsibility. We've made mistakes, but also, who knew a recession was coming?" Bill says.

"We all make mistakes, honey," Lydia says.

Michael J. Fiedler for BI

While Americans on average are saving close to the recommended 15% of their income for retirement, many in their 80s and 90s grew up before financial education and 401(k)s were prevalent. Not saving enough was a common regret among the over 3,800 older Americans who shared with BI their retirement regrets and what aspects of their lives they would redo if they had the chance.

Maura Porcelli, a senior director at the National Council on Aging, says the organization "saw people who thought they had done their due diligence in planning for retirement, the sort who thought their monthly budgets were going to be sufficient, who had all those hopes dashed."

"We know that a good number of older adults are susceptible to a major life event that can knock out a major chunk of their savings," she says.

According to the Federal Reserve's Survey of Consumer Finances, the bottom fifth of households headed by someone 75 and older had a net worth of about $75,000 in 2022, including equity built up in their homes.

For now, the Hindses are bracing for another life-shattering event.

"If I lose her, I don't know what I'm going to do," Bill says. "She feels the same way."

Working to survive and holding on to each other

Some days after work, Lydia sits at her computer and applies for any job she could reasonably do. She tries to appear as sprightly as possible in her applications, sometimes emphasizing how she graduated from the University of Hartford mid-career in 1994. Though she omits her age from her résumé, she suspects that employers have been able to tell, preventing her from landing anything higher-paying than Home Depot.

To counter her many rejections, she started building an online business selling funny gift cards, bags, and clothes. She hired a company to design her website, which cost a few hundred dollars. She works with a print-on-demand company to secure merchandise. She hopes it will take off enough that she can work fewer hours at Home Depot.

Michael J. Fiedler for BI

There is little concrete data about the prevalence of potential ageism among workers in their 80s. Companies are prohibited from age discrimination against workers 40 and older per the Age Discrimination in Employment Act. Many of the dozens of workers BI spoke with say they suspected their age hindered their progress at work or hurt their job applications.

"Managers are already thinking that 60 is too old, so there's little hope for someone who is much older," says Janine Vanderburg, who founded the anti-ageism nonprofit Changing the Narrative. "Many of the job boards for older workers are focused on lower-paid jobs where there's a demand. If you cannot pay your mortgage, your rent, whatever it is, and you need to work, it's better to do something than nothing."

Though programs like the Senior Community Service Employment Program help lower-income Americans 55 and older get job training, the two dozen aging and work researchers and organization executives BI spoke to agreed there should be more resources for older Americans in the workplace. This could include more conversations with workplace leadership about advocating for older workers, more training on technology topics like AI, or local legislation codifying more protections against ageism.

Lydia and Bill hope to move out of their apartment before their rent rises again. It's increased by nearly $300 a month since they moved in 2019, but they have nowhere to go. They're waiting for an open cottage at a nearby care facility, which would cost $1,650 for a one-bedroom unit, but they've rethought whether that would be feasible financially.

"I want to be in a place where if something happens, we're still together — or at least we can visit each other easily," Lydia says. With all the financial strain, some days, Lydia wants to give up and say, "The hell with it."

Michael J. Fiedler for BI

The couple attributes their longevity to their connection. They say they rarely fight, and when they do, it ends with laughs and comfort.

"We're soulmates," Lydia remarks, pointing to Bill.

Their relationship is vital because many people in their community, she says, are not well enough to live active lives. Plus, Lydia no longer speaks to her daughter after years of a souring relationship. Bill's relationship with his children is tighter. For his 90th birthday, most of his family flew to Connecticut. They're about to become great-grandparents.

It's hard to maintain friends on a budget, Bill says. They've set aside some money to visit a friend on Cape Cod in October, and Bill has plans to see a film with a friend. One of the downsides of aging, he says, is losing friends left and right. Many have died, while others have drifted away. Their Christmas dinner table of 10 a few years ago has dwindled to just three.

Amid financial frustrations and loneliness, they find moments of solace. Now and then, they drive the half hour to Hartford in their 2023 Hyundai Elantra for a concert or to the shore with their dog.

But often, it's the little moments that distract them from their financial anxiety. For the first time in five years, Bill sits at the piano in their community's clubhouse. He strikes a few chords, cringing as the notes sound slightly too dissonant for his liking.

"I have perfect pitch," Bill says.

"When I shout, he can tell me what note it is," Lydia whips back.

From memory, he plays selections from Claude Debussy's "Clair de Lune" and Frédéric Chopin's "Nocturnes," missing a note here and there to his frustration. Tears stream down Lydia's face as he serenades her with the out-of-tune piano. When he finishes a prelude, she hugs him tightly.

Michael J. Fiedler for BI

It's moments like these that keep her going, she says, holding his hand on the walk back home. Once there, Lydia takes a green binder and places it on her coffee table. In it are 30 pages of notes in preparation for a September trip to New York City for Bill's 91st birthday.

A dozen pages are devoted to receipts, directions, and other logistics, like a fancy Italian dinner at Carmine's and a $550-a-night hotel room on Broadway. But given their finances, they've canceled the dinner and are just doing a day trip without a hotel stay. They want to save for Lydia's birthday in August.

"I wanted to do something special, but we can't swing it," Lydia says, grabbing a tissue to wipe her eye. "A lot of people don't make it to 91."

One page sticks out. It's a receipt for the Broadway musical "Buena Vista Social Club": Two front-row balcony tickets cost her $700. She's paying $50 a month through November via a buy now, pay later app. Bill has long loved the music, and though the tickets were out of their budget, she says it's worth it. For just a day, they will feel wealthy.

Nothing, not even the medical bills protruding from her desk, her dwindling paystubs, or a dozenth new medication, would get in the way of that.