Published on December 29, 2024 3:17 PM GMT

To many people, the land value tax (LVT) has earned the reputation of being the "perfect tax." In theory, it achieves a rare trifecta: generating government revenue without causing deadweight loss, incentivizing the productive development of land by discouraging unproductive speculation, and disproportionately taxing the wealthy, who tend to own the most valuable land.

That said, I personally think the land value tax is overrated. While I'm not entirely against it—and I think that several of the arguments in favor of it are theoretically valid—I think the merits of the LVT have mostly been exaggerated, and its downsides have largely been ignored or dismissed for terrible reasons. In my view the LVT is at best a useful but highly limited tool ("the worst tax policy ever, except for all the others that have been tried"); at worst, it is a naive proposal that creates many more problems than it solves.

In many ways, the enthusiasm surrounding the LVT seems like it has morphed into a kind of ideological fervor, where it is treated as a universal solution to a wide range of housing and economic problems. In various circles, the LVT has transcended its role as a reasonably sensible tax policy and is instead hailed as some sort of panacea to a disparate set of barely connected issues. This sentiment is epitomized by the meme "Land value tax would solve this", which is often repeated in response to housing-related debates on Twitter.

In this post, I aim to balance this debate by presenting several arguments that challenge the overly optimistic view of the land value tax. To be clear, it is not my aim to provide a neutral analysis of the LVT, weighing up all the pros and cons side-by-side, and coming to a final conclusion about its value. Instead, this post will focus exclusively on some of the most significant arguments against an LVT, which I feel are often ignored by even the most intellectually honest proponents of the LVT.

If you'd like to get a more complete picture of the overall merits of an LVT, in order to assess for yourself whether the negatives of the LVT outweigh the positives, I recommend reading this blog post series on Astral Codex Ten. There you will find a positive defense of Georgism, the philosophy most closely associated with the LVT.

Core problems with the LVT

A fundamental issue with the land value tax lies in the tension between its theoretical appeal and its practical implementation. On paper, the LVT is often presented as an efficient, distortion-free tax that encourages productive land use. However, I argue that this "naive" version of the LVT—the simplest and most commonly proposed form—actually contains intrinsic economic distortions that disincentivize using land efficiently.

Even in the best-case scenario, the naive version of LVT suffers from an inherently narrow tax base, limiting the revenue it can generate. Attempts to address its flaws, as outlined below, would further erode this already-limited tax base while also making the proposal significantly more complex, both administratively and legally. These issues ultimately undermine the practicality and effectiveness of the LVT as a policy tool.

An LVT discourages searching for new uses of land

Perhaps the most significant drawback of the land value tax is that it inherently discourages landowners from searching for new and innovative uses for their land. This stems from the fact that if a landowner successfully discovers a valuable resource or identifies a creative way to utilize their land more productively, the government will increase their tax burden accordingly. In other words, the moment a new use or resource is discovered, the land’s "unimproved value" rises, and the landowner is immediately penalized with a higher tax bill.

Take, for example, the case of surveying land for oil. Imagine a landowner invests significant time, money, and effort into exploring their property to determine whether it contains untapped oil reserves. If they do find oil, the value of their land would skyrocket because the presence of oil dramatically increases its economic potential. However, under an LVT system, this increased value does not benefit the landowner in the way it traditionally would. Instead, the government essentially "seizes" the added value by taxing its rental value away, eliminating the incentive to discover the oil in the first place. This happens regardless of the landowner’s investment in the exploration or the associated risks they took to find the oil.

This disincentive to search for new ways to use land is intrinsic to the land value tax: since a landowner does not actually create the oil on their land, but merely discovers it, the oil would be part of the land's "unimproved value", which is inherently subject to taxation under the LVT.

As far as I can tell, this argument was first given by Zachary Gochenour and Bryan Caplan in 2012. As Bryan Caplan argued,

You might think that this is merely a problem for a handful of industries. But that’s probably false. All firms engage in search, whether or not they explicitly account for it. Take a real estate developer. One of his main functions is to find valuable new ways to use existing land. “This would be a great place for a new housing development.” “This would be a perfect location for a Chinese restaurant.” And so on.

An LVT implicitly taxes improvements to nearby land

Another issue with the LVT is that it acts as an implicit tax on nearby land development.

To understand why, consider that the value of unimproved land tends to increase whenever nearby land is developed. For example, if someone builds new infrastructure, housing, or businesses on neighboring plots of land, the surrounding area becomes more desirable and valuable as a result due to network effects and proximity. Under a land value tax, this rise in land value would lead to higher taxes for the owners of nearby, unimproved plots—even though they themselves did nothing to cause the increase.

This is important because it implies that, under an LVT, landowners with large plots of land are disincentivized to create any improvements they make to one part of their property, as it could trigger higher taxes on nearby land that they own. For instance, if a developer owns multiple adjacent parcels and decides to build housing or infrastructure on one of them, the value of the undeveloped parcels will rise due to their proximity to the improvements. As a result, the developer faces higher taxes on the remaining undeveloped land, making development less financially appealing in the first place.

This creates a counterproductive dynamic: developers may hesitate to improve their land or invest in new projects because they know that any improvements will increase their tax burden on adjacent parcels. Instead of encouraging development, as LVT proponents often claim, this dynamic can actually discourage it, particularly for those who own large amounts of land in a given area. In this way, the LVT could unintentionally slow down the pace of development and undermine one of its supposed benefits—promoting more productive land use.

I first learned about this critique of the LVT from the The Concise Encyclopedia of Economics by Charles Hooper. He explains,

George was right that other taxes may have stronger disincentives, but economists now recognize that the single land tax is not innocent, either. Site values are created, not intrinsic. Why else would land in Tokyo be worth so much more than land in Mississippi? A tax on the value of a site is really a tax on productive potential, which is a result of improvements to land in the area. Henry George’s proposed tax on one piece of land is, in effect, based on the improvements made to the neighboring land.

And what if you are your “neighbor”? What if you buy a large expanse of land and raise the value of one portion of it by improving the surrounding land. Then you are taxed based on your improvements. This is not far-fetched. It is precisely what the Disney Corporation did in Florida. Disney bought up large amounts of land around the area where it planned to build Disney World, and then made this surrounding land more valuable by building Disney World. Had George’s single tax on land been in existence, Disney might never have made the investment. So, contrary to George’s reasoning, even a tax on unimproved land reduces incentives.

Can't the LVT simply be patched to address these issues?

Supporters of the land value tax have, of course, responded to these critiques by suggesting that patches could be introduced to address its flaws.

Typically, these suggestions modify the simple uniform LVT proposal—which simply taxes unimproved land value (the "naive" LVT)—by incorporating tax exemptions, deductions, or other stipulations to prevent unintended consequences.

For instance, to solve the problem that an LVT eliminates the incentive to search for better uses of land, some proponents suggest that a well-designed LVT could include compensation for landowners who invest time and resources into discovering more efficient or productive ways to utilize their land. Similarly, to address the criticism that the LVT discourages development by large landowners—since improvements on one parcel of land raise taxes on nearby parcels they own—governments could offer tax reductions or exemptions to developers who improve a significant amount of land within a single geographic area. This could offset the disincentive effect for those most affected.

However, these proposed fixes fail to address a deeper and more fundamental issue: adding such patches to the LVT fundamentally undermines its ability to function as a substantial source of tax revenue.

Even in its simplest "naive" form, the LVT has a narrow tax base. The reality is that the vast majority of global wealth is created through human labor and innovation, not through the inherent value of natural or undeveloped land. If this sounds counterintuitive to you, perhaps imagine being transported to Earth millions of years ago, before humans evolved. Being the only human on Earth, you'd "own" all the natural resources on the planet, but you'd be unable to access almost any of the value tied up in those resources, because unlocking that value requires human labor and tools that haven't been invented yet.

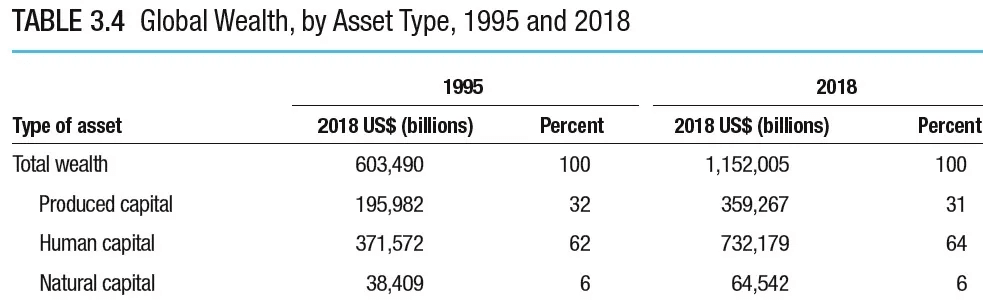

To get more quantitative, the World Bank estimates only about 6% of the world's total wealth comes from "natural capital": the specific type of wealth that the LVT is designed to target.

By introducing exemptions, compensations, or other stipulations meant to address its shortcomings, the LVT’s tax base would likely shrink even further, below this estimate of 6%. This could render the tax financially insignificant, defeating its purpose as a meaningful revenue source. In trying to fix the distortions of a straightforward LVT, policymakers would risk eroding the tax’s core economic viability altogether.

Moreover, these fixes would introduce significant complexity into the tax system, undermining the LVT’s reputation as a simple and efficient tax. Take, for instance, the proposal to compensate landowners for uncovering better uses of their land. To implement such a measure, governments would need to assess how much of a land's value increase is attributable to the landowner's discovery efforts versus external factors, such as improvements in surrounding infrastructure, or changes in market conditions. These assessments would require intricate and subjective valuations that are very difficult to quantify accurately.

This kind of patch could easily result in a bureaucratic nightmare. It would necessitate the creation of complex appraisal mechanisms to evaluate each individual case, demanding significant administrative resources and expertise. Ensuring that these evaluations are accurate, consistent, and transparent would be an enormous challenge, and the process would inevitably be prone to errors, costly legal disputes, and political manipulation.

Governments would likely struggle to reliably make these determinations without introducing distortions to the market. Moreover, risk-averse investors would likely be discouraged from getting involved with such a system, as it would become more difficult to reliably predict the outcome of disputes. These dynamics undermine the core claim among supporters of an LVT that an LVT would generate "no deadweight loss".

The second proposed patch—to offer tax breaks or exemptions to large land developers who improve nearby tracts of land—comes with its own set of problems. While it might address concerns about discouraging development, this approach would disproportionately benefit large-scale developers and wealthy landowners who hold vast amounts of land. As a result, this adjustment would undermine one of the LVT's central selling points: the idea that it hits the richest landowners the hardest.

The government has incentives to inflate their estimates of the value of unimproved land

The implementation of a land value tax also seems likely to create incentives for governments to expand the scope of the tax, rather than limiting its application purely to unimproved land. This makes sense in light of public choice theory, which views government actors—whether elected officials, bureaucrats, or tax assessors—as largely self-interested actors, rather than benevolent and unbiased actors solely interested in the public good.

The key issue here lies in the inherent difficulty of appraising the value of "unimproved" land. Determining the value of land without accounting for the structures, artificial modifications, or other improvements on it is far from straightforward. Appraisers would need to disentangle the natural value of the land itself from the value added by human effort, investment, or potentially nearby development. This process is not only subjective but also ripe for errors, inconsistencies, and manipulation. Politicians or government workers, motivated by the need to maximize revenue, would have a strong incentive to discover a mechanism to push these appraisals higher, claiming that much of the land's value is technically "unimproved" and thus taxable under the LVT.

As just one illustrative example, tax assessors could, for instance, argue that farmland made fertile by decades of manmade irrigation is now part of the land’s "natural" value, thereby expanding the taxable base.

A sufficiently carefully designed LVT could help to mitigate these issues, for example by severely restricting the discretion that government workers have over the appraisal process, and by requiring that neutral third parties review all procedures to ensure that estimates are unbiased and fair. However, in light of some of the previous arguments that I have given in this essay—particularly the fact that an LVT would require a complex appraisal system to avoid disincentivizing the discovery of new ways to use land productively—it seems very difficult to create a system that would be free from manipulation. Therefore, it seems very hard to be confident that implementing an LVT would have the advertised effect of creating no new disincentives for land development.

An LVT is unlikely to replace many existing taxes

Given the political incentives involved, and the fact that a land value tax has an inherently small tax base, the LVT is unlikely to fully replace existing taxes, such as income, sales, or property taxes. Instead, it would likely be added on top of these existing revenue streams. Governments are typically reluctant to eliminate major sources of revenue, especially those that have been entrenched for decades. As a result, the introduction of an LVT would likely not represent a clean substitution but rather an additional layer of taxation.

This significantly undermines one of the core arguments in favor of the LVT: its potential to increase economic efficiency. The theoretical benefit that an LVT could reduce deadweight losses is contingent on it replacing less efficient taxes that distort economic activity. However, if the LVT mostly just supplements existing taxes, its efficiency gains would be muted, if they even exist at all. Businesses and individuals would still face the distortions caused by income and sales taxes, while also shouldering the added burden of the LVT. In such a scenario, the tax system as a whole could become more complex and less efficient, negating many of the theoretical advantages proponents claim for the LVT.

Disruptions under the LVT

The precedent set by a full LVT

Another major issue is that a full or near-full land value tax would likely establish a troubling precedent by signaling that the government has the appetite to effectively confiscate an additional category of assets that people have already acquired long ago through their labor and purchases.

The concern here—which, to be clear, is not unique to the LVT—is that the introduction of an LVT set at a high rate (especially near 100%) would likely erode confidence in property rights, discouraging individuals and businesses from engaging in wealth creation and long-term investment, as they think their wealth could one day be seized, just as easily as the LVT was imposed.

To elaborate, people currently operate under the assumption that the government will not arbitrarily take away certain types of property they have legally acquired. This assumption is foundational to economic planning and investment. For instance, individuals buy stocks, businesses invest in capital goods like machinery, and developers improve real estate—all with the expectation that they will retain most of the value of their assets and any future returns from them. This confidence in the protection of property rights encourages entrepreneurship, innovation, and economic growth.

However, people are generally sensitive to any indication that this assumption may no longer hold in the future. If a government suddenly and unexpectedly began taxing the full rental value of unimproved land—an asset previously considered part of an individual's property—it would likely send a signal that property rights are less secure than they were believed to be.

Even if the government explicitly frames the policy as a unique case that applies only to the unimproved value of land, many people would view this as a convenient post-hoc justification for changing the rules. This is because, for much of history, the value of unimproved land has been treated as a legitimate part of private property, and this is particularly true in the United States compared to other countries. Indeed, many people in the US have long held that the land they own is a core part of the concept of private property. Abruptly revoking this understanding would be perceived as a modification of the government’s prior commitments to protecting property rights.

This perception matters because it leads people to rationally update their expectations about the government's future behavior. If the government can justify taxing away the full rental value of unimproved land today, what assurance is there that it won’t expand its confiscatory policies in the future? The worry here is that such a shift in policy could make people fear that other forms of easily-taxable property—such as capital goods or financial investments—might also be targeted in the future, albeit with different excuses offered by the government for why they reneged on what was perceived as their previous commitments. Even if no such additional policies are planned, the uncertainty created by the introduction of an LVT could discourage individuals from acquiring or developing assets that they think might be confiscated from them in the future, thereby reducing overall economic productivity and wealth creation.

Furthermore, this precedent would likely disproportionately affect perceptions regarding permanent assets that are easier to confiscate, like durable physical capital, while leaving more temporary or ephemeral goods like consumption goods relatively unaffected. This seems likely to shift people's financial habits towards higher levels of consumption at the expense of savings and investment. Under standard models of economic growth, such a shift would have the effect of reducing long-term prosperity.

An LVT would massively disrupt millions of people's long-term plans

Beyond setting a harmful precedent that could influence people's future behavior, a land value tax also creates a major disruption to people's current financial plans, particularly for those who have spent decades developing strategies to preserve their wealth. Millions of individuals and families have purchased land with the understanding that its value would remain secure and that it would not be subject to confiscatory taxation. The introduction of a full LVT fundamentally alters this assumption, effectively pulling the rug out from under those who relied on the previous system when making long-term financial decisions.

This disruption is not simply a matter of fairness—I am not simply saying that it is unfair that the LVT takes money from some people and redistributes it to other people. Almost every government policy has both winners and losers, and I am not merely saying that since this policy has losers too, it should therefore be avoided. Instead, my core argument here is that this sudden shift is economically inefficient, as it forces people to spend time and resources adapting to new circumstances unnecessarily.

The scale of such a disruption would be enormous. In the United States, tens of millions of people own significant amounts of land—whether as part of a retirement strategy, for generational wealth preservation, or as an asset to be used for future financial stability. These people spent potentially thousands of hours of their life building a sound financial strategy to provide for themselves and their children, and would see the fruits of their efforts substantially dissipate in light of a burdensome LVT.

For example, retirees who bought land years ago often rely on its value as a key part of their retirement strategy, whether to sell it in the future or to pass it on to their heirs. An LVT forces them to suddenly adapt to an entirely new environment, where the land they own is no longer a stable or predictable asset but instead becomes an ongoing financial liability due to the recurring tax burden.

This abrupt transition seems likely to be quite costly, both on an individual and a societal level. Individuals who previously planned to use their land for wealth preservation would now have to scramble to find alternative strategies. For elderly retirees, this shift would be particularly harmful to their economic welfare, as these people typically have less cognitive flexibility to adapt to abrupt changes in their financial environment.

The purported effect of an LVT on unproductive land speculation seems exaggerated

One of the central arguments made by proponents of the land value tax is that it would discourage individuals from holding onto land in anticipation of its value appreciating over time, rather than putting the land to productive use. The idea is that by taxing the unimproved value of land, the LVT would eliminate the financial incentive to keep land idle and force landowners to either develop it or sell it to someone who will.

However, this argument depends on a questionable model of how land speculation works. Specifically, it assumes that pure land speculation—simply holding onto land and doing nothing with it—is more profitable than selling the land to a developer and reinvesting the proceeds elsewhere. This assumption strikes me as dubious.

In reality, the opportunity cost of holding idle land is not insignificant. When a landowner holds onto undeveloped land, they forgo the potential income they could have earned by selling it and investing the money into other productive assets, such as stocks, bonds, or real estate developments elsewhere. Economic theory suggests that rational landowners would compare the expected appreciation of their land to the returns they could earn from reinvesting their capital, and in most cases, holding idle land for an extended period of time would likely not be the most profitable option.

Even in cases where land is held idle by developers or investors, it is unclear that speculation is inherently harmful or inefficient in an economic sense. Land speculation often involves anticipating future trends in development, infrastructure, or zoning, and holding land can sometimes be a rational way to align its use with long-term economic needs. For example, an investor who buys land near a growing city may be waiting for the right moment to develop it, ensuring that the land's use aligns with future demand. The act of holding land in such scenarios could be seen as part of a broader rational economic process, rather than as an inefficiency that needs to be corrected.

Moreover, there is often a simple alternative explanation for why land often appears to be held idle even when regulations allow the owners to sell it to developers. This explanation comes down to sentimental attachment.

Many landowners may simply have a deep emotional connection to their land, which makes them reluctant to sell, even if doing so might be financially advantageous. For example, someone who has inherited land that has been in their family for generations may view it as a legacy or a symbol of their heritage, rather than as a purely financial asset. In such cases, the decision to hold onto the land is driven not by speculative motives but by personal values that outweigh financial considerations.

This explanation strikes me as more plausible in many cases than the speculative model assumed by LVT supporters. Unlike professional developers or large corporations, individual landowners with sentimental ties to their property are not necessarily looking to maximize profit. Therefore, taxing the unimproved value of their land through an LVT would not necessarily compel them to sell or develop it. Instead, it might simply place an additional financial burden on individuals who already have strong personal reasons for holding onto their land, doing little to incentivize the creation of additional housing developments.

Final words

While I spent this entire post critiquing it, I'd like to reiterate that I don’t think the land value tax is entirely without merit. While the arguments I’ve outlined above personally make me feel that the LVT is far less appealing than many of its proponents claim, this doesn’t mean the tax is necessarily worse than other alternatives, such as corporate income taxes or wealth taxes, which also come with their own serious drawbacks.

In my view, the LVT should be seen as just one flawed tool among many that governments can use to raise revenue. It may well be less flawed than many other tax policies, but that doesn’t make it very good by itself. My point is simply that its limitations and practical challenges mean that it is far from the panacea its strongest advocates make it out to be.

Discuss